Last updated on June 25th, 2026 at 07:04 am

Budgeting as a couple means creating a shared plan for how you and your partner earn, spend, save, and grow your money together — while still making sure neither of you loses your financial footing in the process.

If you’ve ever had a tense moment over a credit card statement — or a “we need to talk about our spending” conversation that went nowhere — you’re not alone. That’s just what happens when two people with different money habits try to share a life without a clear system.

This guide covers the three main budgeting models, how to split expenses fairly when incomes aren’t equal, and how to talk about money without it turning into a fight.

Why Budgeting as a Couple Feels So Hard (Even When You’re Both Responsible)

Managing money alone is already personal. Managing it with someone else means navigating two different money histories, habits, and comfort levels — and that combination makes couple finances genuinely complicated.

If money was tight growing up, you might be an aggressive saver who panics at any credit card balance. If your partner grew up more comfortably, they might spend freely without much worry. Neither is wrong — but without a shared system, those differences create friction over time.

The most common couple money anxieties — and why they’re valid:

| What they say | What’s really going on |

|---|---|

| “Who pays what?” | No clear system — someone feels like they’re doing more |

| “We have different spending habits” | Different money histories colliding in the present |

| “I don’t want to lose my independence” | Fear that merging finances means losing autonomy |

| “One of us earns more — is that fair?” | Income gap creating an unspoken power imbalance |

| “I’m embarrassed about my debt” | Financial shame making honesty feel risky |

| “We want different things” | Misaligned goals neither person has named yet |

Every one of those anxieties is workable. None require identical incomes or identical habits — just clarity about what you each want, what you each bring, and what you’re working toward together.

The Three Budgeting Models — And How to Pick the Right One

There’s no single “correct” way to budget as a couple. What works brilliantly for one relationship can feel suffocating or chaotic for another, and that’s completely expected. Most couples land on one of three models — or a blend of them.

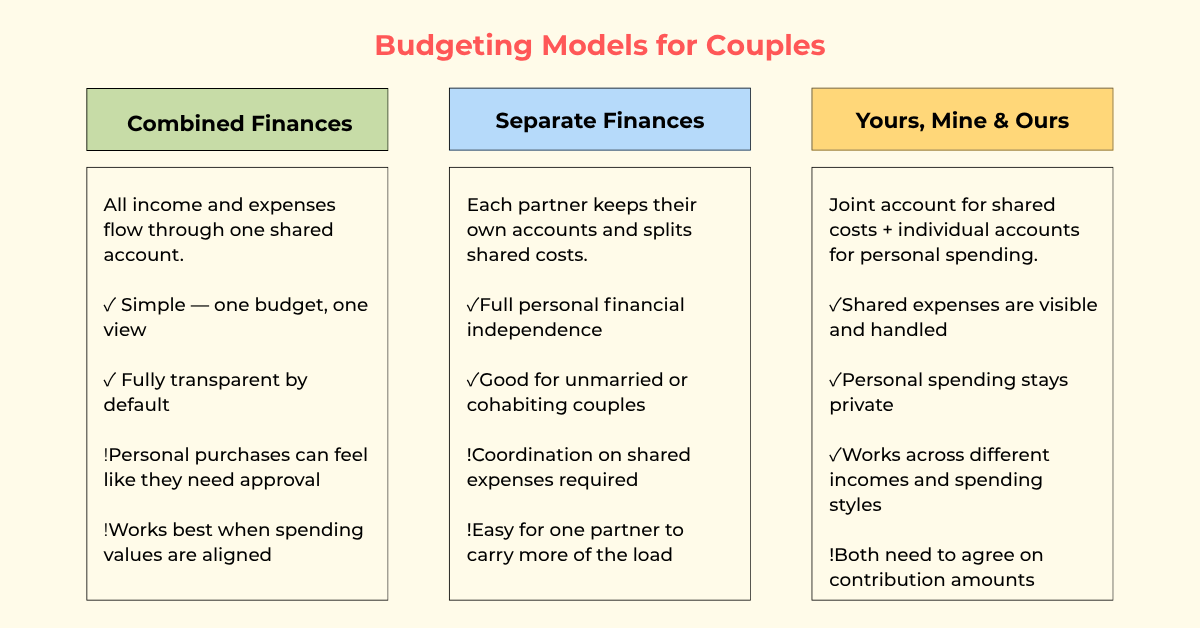

Model 1: Combined Finances (The All-In-One Approach)

Every dollar flows through one shared budget. Both incomes come in, all expenses go out, and everything is tracked together in one place.

How it works:

- Both partners deposit income into one joint account

- All household expenses — rent, groceries, utilities, dining, entertainment — come out of that account

- Savings goals are funded together

- There’s one budget, one view, and full financial transparency

Best for: Couples who are fully aligned on spending values and comfortable with total financial visibility.

This is actually how my parents have always done it. My dad hands over 100% of his income, and my mom manages everything — the bills, the savings, the budget. It works for them because there’s complete trust, and my mom genuinely enjoys handling the finances. But it only works because both of them agreed to it. If either one had reservations, the same setup would feel very different.

The honest challenge: When every transaction is technically shared, buying something personal — a $50 book, a new pair of shoes, a gadget your partner finds unnecessary — can start to feel like it needs sign-off. For people who value individual financial autonomy, that friction wears on them over time.

Model 2: Separate Finances (The Independent Approach)

Both partners keep their own accounts, agree on how to split shared expenses, and manage everything else independently.

How it works:

- Each partner keeps their own income, savings, and spending account

- Shared expenses (rent, utilities, groceries) are split by a pre-agreed method — usually 50/50 or proportional

- Personal spending is completely independent

Best for: Unmarried couples, couples who prefer financial autonomy, or partners who came into the relationship with established financial lives they want to keep intact.

The honest challenge: Without a clear system, the “who owes who what” math gets old quickly. One person often ends up managing most of the financial coordination, which creates a different kind of imbalance.

Model 3: The “Yours, Mine, and Ours” Hybrid System

This is the model that tends to work for the widest range of couples — and it’s the one that consistently comes up when financially stable couples describe what they actually do.

How it works:

- Both partners contribute to one joint account for all shared household expenses

- Each partner keeps their own individual account for personal spending

- Personal spending from individual accounts requires no explanation or justification

- Contribution amounts to the joint account are either equal (50/50) or proportional to income

Best for: Couples with different spending styles, couples where one partner earns more, or anyone who wants full transparency on shared expenses without losing personal financial freedom.

Which Model Is Right for You?

| Combined | Separate | Hybrid ★ | |

|---|---|---|---|

| Transparency | Full | Varies | Shared: full · Personal: private |

| Autonomy | Low | High | Balanced |

| Coordination needed | Low | High | Medium |

| Best for | Married, fully aligned | Unmarried or cohabiting | Most couples |

Not sure which model fits? Start with the hybrid. It’s the most flexible, adjustable as you go, and it directly solves the “who pays what” question without requiring a full financial merger.

How to Have the Money Conversation (Without It Turning Into a Fight)

Most couples wait until there’s a problem before talking about money — a surprise bill, a savings account that hasn’t moved in months. By then, the conversation arrives loaded with stress.

A better approach: normalize talking about money before anything urgent forces it. Not a formal sit-down — just an honest “here’s where I’m at” conversation.

If both people are open about money as a general habit, whether you use joint or separate accounts barely matters. Transparency is the foundation. The account setup is just logistics on top of it.

What to cover in your first real money talk:

- Income — What each of you earns, including side income, freelance, or investment income

- Fixed expenses — Rent or mortgage, loan payments, insurance, recurring subscriptions

- Variable spending — Food, dining, entertainment, personal spending. Pull up actual bank statements instead of guessing — most people underestimate this category significantly

- Debt — Student loans, car payments, credit cards. Not just the balance, but the interest rate and payoff timeline

- Financial goals — What you each want in the next 1, 3, and 10 years — and whether those actually line up. A goal doesn’t have to be a house or a retirement fund to count. My boyfriend works overseas, so every month we set aside a fixed amount into what we call our “date fund” — money that just sits there until he’s home and we can actually use it together. It’s one of the simplest things we do financially, but it works because we both know what it’s for and we both leave it alone until then. That’s really what a named goal does: it removes the temptation to dip into it for something else.

- Money stress triggers — If your partner panics at the sight of any credit card balance and you’re fine sitting with one while building savings, that tension is worth naming now

That last one gets skipped most often. But knowing what financial stress looks like for your partner — not just what they spend, but how they feel about money — is genuinely useful information when you’re building a life together.

One thing that holds true across all setups: If both people are honest and forthcoming about finances as a general habit, whether you use joint accounts or separate ones barely matters. The structure helps with management. The honesty is what actually holds everything together.

If you want to take it a step further, loud budgeting is a trend worth knowing about — it’s essentially the practice of being openly vocal about your finances, which can actually make couple budgeting a lot easier.

How to Build Your Couple’s Budget — Step by Step

Once the conversation’s happened, it’s time to build the actual system. If you’re still figuring out which approach works for you, this guide on different budgeting strategies covers the most common frameworks side by side.

Add up your combined income

List all take-home income for both partners — salaries, side income, freelance, anything regular. Use your average monthly take-home, not your gross salary.

List all fixed expenses

Rent or mortgage, loan payments, insurance, subscriptions, phone plans. Add them up — this is your monthly floor before anything else happens.

Estimate variable spending with real numbers

Pull up three months of actual bank and credit card statements. Groceries, dining, entertainment, clothing, transport. Most couples find they’re spending more than they estimated here.

Apply the 50/30/20 rule as a starting point

A reliable framework for allocating income. Treat the percentages as a direction, not a strict grade.

Set shared goals with real numbers

“We want to save $18,000 for a house down payment by next December” is something you can build around. “We want to save more” isn’t.

Decide who tracks what

Split budgeting responsibilities in a way that works for both of you, then review your finances together each month.

How to Split Expenses When One of You Earns More

The 50/50 split sounds fair on paper. But when one partner earns $6,500 a month and the other earns $2,500, an equal split quietly builds resentment on both sides — one partner perpetually stretched thin, the other feeling like they’re carrying everything.

The proportional split is the more equitable alternative.

How it works:

Each partner contributes to shared expenses based on their percentage of combined household income.

Example:

Both contribute. Neither carries a disproportionate burden.

If one partner earns money and the other runs the household, both are doing real work. That’s why it’s important for each person to have their own spending money built into the budget — no explanations needed. Relying on “just ask me if you need something” creates a very different (and less equal) dynamic.

The Monthly Money Date

The setup gets all the attention, but the check-in is what keeps a budgeting system alive over time.

A money date is a regular, scheduled time — ideally monthly — where both of you sit down and look at the numbers together. No ambushes, no surprises. Just a calm and expected conversation that both people show up for.

Couples who build this habit early — especially during the newlywed or cohabiting phase — tend to have fewer money arguments later on. Not because money gets easier, but because the conversation has a regular home.

💡 If you’re looking to understand budgeting better, take a look at our guides and tools for managing your money.

Explore Budgeting Calculators & GuidesJoint vs. Separate Accounts — What Actually Makes Sense

The joint vs. separate account debate is one of the most common questions couples ask, and the honest answer is: it depends on your model.

| Account Setup | Works Best With | Watch Out For |

|---|---|---|

| One joint account for everything | Combined finances model | Loss of individual autonomy |

| Completely separate accounts | Separate finances model | Active coordination; unequal mental load |

| Joint + individual accounts | Hybrid model | Both need to agree on contribution amounts |

| Joint + joint savings + individual | Comprehensive hybrid | More accounts to manage, but maximum flexibility |

The non-negotiable: Both partners need full visibility into the shared finances. A joint budget that only one person tracks isn’t a joint budget.

Not sure how to structure multiple accounts? Here’s a guide on how to budget with multiple bank accounts.

Budgeting at Different Stages of Your Relationship

A budget for a couple who just moved in together looks genuinely different from one managing a mortgage, two kids, and retirement accounts. The system should evolve with your life.

Before Marriage / Moving In Together

This is the stage for building the foundation. Focus on:

- Getting honest about what debt each person is carrying

- Deciding how to split shared expenses (proportional vs. 50/50)

- Opening accounts that fit your chosen model

- Having the first real money conversation before a crisis forces it

For most unmarried couples, the hybrid model is the easiest entry point — no full financial merging required, and it’s easy to adjust as the relationship evolves.

Newly Married / Just Combined Households

The newlywed budget tends to involve:

- Consolidating or restructuring accounts

- Setting joint financial goals for the first time

- Managing lifestyle inflation — combined income can feel like a windfall, and spending tends to rise to match it

- Establishing the money date habit before life gets complicated

Getting the monthly check-in in place during year one is genuinely valuable. Maintaining an existing habit is far easier than starting one after years without it.

Established Couples With Kids or a Mortgage

The budget gets considerably more complex here:

- Childcare and education costs

- Home maintenance (budget roughly 1% of home value annually)

- Larger emergency fund — ideally 6 months of expenses when you have dependents

- Life insurance and basic estate planning

- Retirement contributions for both partners

This is the stage where working with a [fee-only financial advisor] makes the most sense — particularly for long-term wealth building, retirement projections, and protecting the financial future of the family.

Long-Term Partners (10+ Years)

Financial habits solidify over time, for better or worse. A long-term couple doesn’t need to overhaul everything — but a once-a-year review asking “does this system still fit our actual life?” is worth doing. Goals change. Income changes. Priorities shift. The system should shift with them.

Real-Life Scenarios: What Other Couples Actually Do

These aren’t prescriptions — just examples of how different couples have made things work in practice.

Scenario 1: Equal earners, hybrid model

Both partners earn roughly the same. They each put $1,500/month into a joint account for rent, groceries, utilities, and shared subscriptions. The rest stays in individual accounts for personal spending — no questions asked. They meet monthly to review the joint account together.

Scenario 2: Significant income gap, proportional split

Partner A earns $5,000/month, Partner B earns $2,000/month. They contribute to shared expenses proportionally — Partner A covers 71%, Partner B covers 29%. Both get the same personal spending budget each month. Neither feels like a financial burden to the other.

Scenario 3: One working partner, stay-at-home parent

The working partner’s income funds the entire household. They’ve agreed that both partners receive a monthly personal spending amount — the same amount — that neither has to explain. The stay-at-home partner has their own debit card, their own spending money, and full visibility into the household accounts.

Scenario 4: Newly cohabiting, not yet married

They keep separate accounts but opened one joint checking account for shared bills — rent, utilities, and streaming. Both contribute $800/month. Personal finances stay completely separate. The monthly review covers only the joint account, so there are no “who owes who” conversations.

The One Thing That Actually Makes It Work

You can set up the perfect system — the right model, the right accounts, the right app, a clean proportional split — and still end up arguing about money if the underlying honesty isn’t there.

The couples who manage money well over the long term aren’t necessarily the ones with the most sophisticated setup. They’re the ones who’ve made it normal to talk about money, without shame, without defensiveness, and without it becoming a referendum on someone’s character. Just a regular part of how they operate together.