Last updated on June 21st, 2026 at 10:25 am

If you have ever had a car break down, a medical bill arrive without warning, or a job end before you were ready, you already understand what an emergency fund is for. It is the money that stands between a stressful surprise and a financial crisis.

I learned this firsthand. After leaving my first corporate job just three days in, I had no savings buffer. I had been doing odd jobs — tutoring, online surveys — but nothing consistent. A few weeks later, my car’s check engine light came on and I had nothing set aside to cover repairs. I had to borrow, stress, and scramble in a way I never wanted to repeat.

That experience was the start of my emergency fund. This guide covers everything I learned along the way: how much to save, where to keep it, how to build it on a limited income, and when it is actually appropriate to use it.

Know What an Emergency Fund Is

You need an emergency fund for unexpected expenses. This is money you should not touch unless it is really needed. It helps you stay calm when life surprises you. Experts say you should have at least 3 to 6 months of your living expenses saved.

At first, I didn’t have any separate fund for emergencies. My savings and emergency money were the same. Later, I learned how important it is to keep it separate so I could feel safer and more in control.

How Much Should Be in Your Emergency Fund?

Most financial experts recommend saving between three and six months of essential living expenses. Essential expenses include rent or mortgage, utilities, groceries, transport, insurance, and any minimum debt payments. Discretionary spending — dining out, subscriptions, entertainment — does not factor into the calculation.

A practical example: If your essential monthly expenses total $2,500, your emergency fund target is between $7,500 (three months) and $15,000 (six months).

How much you should aim for depends on your situation:

- Three months is a reasonable starting target for people with stable employment, dual household income, and low financial dependents

- Six months is more appropriate for freelancers, self-employed individuals, single-income households, people in volatile industries, or anyone supporting dependents

- Some people in high-risk employment situations save up to twelve months of expenses, though three to six months is the widely accepted standard

If six months feels impossibly far away, start with a smaller milestone. A first goal of $500 or $1,000 is meaningful — it covers most minor emergencies and gives you a foundation to build from.

When I started, I saved 10 percent of my income each payday without a specific target in mind. Once I started tracking my monthly expenses properly, I calculated my average and multiplied by six. That number became my real goal. Having a concrete figure made the whole process feel more deliberate.

💡 Not sure how much to save? Use the calculator to estimate your emergency fund based on your monthly expenses.

Try the Emergency Fund CalculatorWhere to Keep Your Emergency Fund

The right place to keep an emergency fund has two requirements: the money must be safe, and you must be able to access it quickly without penalties. Investment accounts, retirement funds, and anything subject to market fluctuation are not appropriate options because the value can drop exactly when you need the money most.

Here are the most common options, with the trade-offs for each:

| Account Type | Accessibility | Interest Potential | Best For |

|---|---|---|---|

| Traditional savings account | High — ATM and branch access | Low (0.01–0.5%) | People who prefer in-person banking |

| High-yield savings account | High — online or app access | Medium (3–5%+) | Maximising growth while keeping funds accessible |

| Digital bank savings account | High — mobile app | Medium to high | Tech-comfortable savers who want higher rates |

| Money market account | High — cheque or debit access | Medium | Those who want slightly higher returns with flexibility |

| Cash on hand | Immediate | None | Small buffer only — not suitable as a primary fund |

Avoid keeping your emergency fund in a checking account you use daily. The friction of a separate account — even a minor one — reduces the likelihood of spending it accidentally.

I started with a traditional bank account because it was familiar. A year in, I moved everything to a digital bank. The interest rate was higher, the app made it easy to check my balance without visiting a branch, and transfers to my main account when I genuinely needed funds took less than a day.

How to Build Your Emergency Fund on a Tight Budget

The most common reason people delay building an emergency fund is that they feel they do not have enough money to save. The more useful framing: you start with whatever is available right now, and you increase it as your income or expenses allow.

Start with a fixed, automatic transfer. Set up a recurring transfer from your main account to your emergency fund on the day you get paid. Even $25 or $50 per paycheck builds the habit and adds up faster than most people expect. Automation removes the decision from the equation entirely.

Use the pay-yourself-first approach. Transfer to savings before spending on anything discretionary. Treat it as a non-negotiable line in your budget. When the money is moved before you have a chance to spend it, it stops feeling like something you are giving up.

Apply windfalls directly to the fund. Tax refunds, work bonuses, gifts, or any unexpected income can accelerate your progress significantly if they go straight to savings before they integrate into your spending. A single $500 windfall can represent weeks of regular contributions.

Look for spending categories to reduce temporarily. This does not mean cutting everything — it means identifying one or two areas where spending is higher than necessary and redirecting that difference to savings. Common examples include food delivery, unused subscriptions, and impulse purchases. Even $30–$50 per month redirected to savings adds $360–$600 over a year.

I started with small fixed amounts each payday and increased them gradually as I tracked my expenses and found room. The automatic transfer was the single change that made saving consistent instead of occasional.

How to Manage Cash Flow While Building Your Fund

Saving consistently requires knowing where your money goes. Without that visibility, it is easy to feel like there is nothing left to save even when there is.

Track your spending for at least one month before setting a savings amount. Most people significantly underestimate how much they spend in variable categories like food, entertainment, and convenience purchases. Seeing the actual numbers often reveals more room than expected.

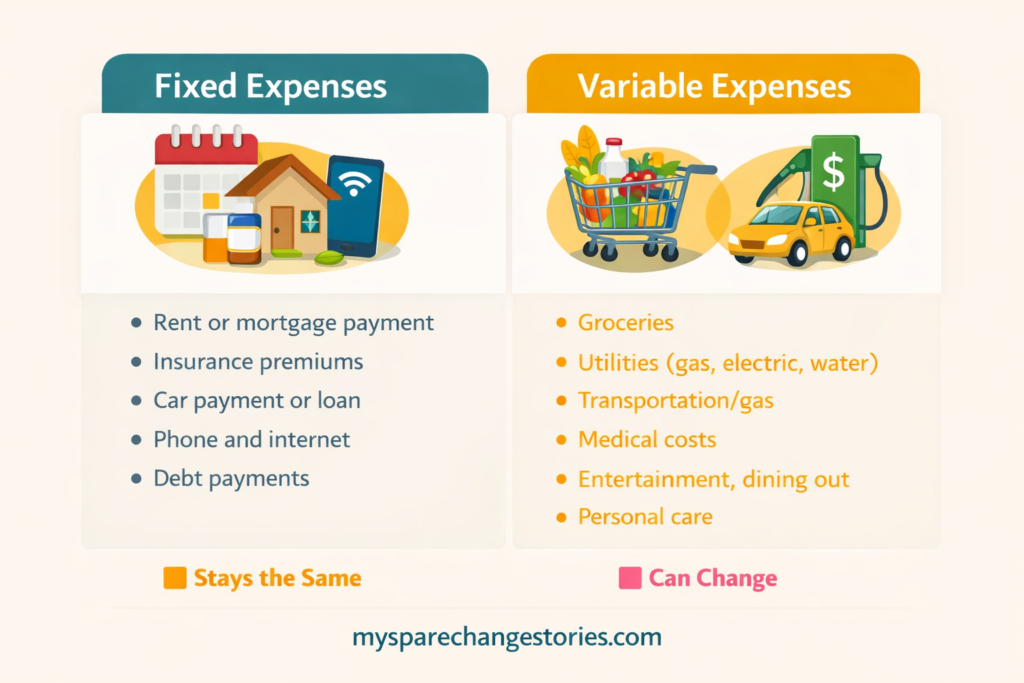

Identify your fixed and variable expenses separately. Fixed expenses — rent, utilities, insurance, subscriptions, loan payments — happen on a schedule and at a predictable amount. Variable expenses shift month to month and are usually where the most adjustable spending lives.

Look for the high-frequency, low-awareness purchases first. Daily coffee runs, food delivery fees, bottled drinks, and impulse add-ons are easy to overlook individually but accumulate quickly. A $6 daily purchase five days a week is $1,560 a year.

When I started tracking expenses seriously, I realized I was spending significantly more on food delivery than I had estimated. Reducing that one category gave me enough margin to increase my emergency fund contributions without changing much else.

Stay Motivated

Saving money can sometimes feel like a slow journey, but don’t lose heart. Watching your savings grow little by little can be surprisingly motivating. Just think about the peace of mind you’ll feel knowing you’ve got a safety net for unexpected emergencies.

What helped me was setting small, achievable goals. Every time I hit one of those milestones, I felt a real sense of accomplishment. It’s a good reminder that even small wins add up and keep you moving forward.

What Counts as a Real Emergency (and What Does Not)

Defining this in advance matters. Without a clear boundary, the fund gets used for non-emergencies and loses its purpose.

These qualify as real emergencies:

- Unexpected job loss or significant reduction in income

- Medical or dental expenses not covered by insurance

- Essential car repair needed to get to work

- Urgent home repair that affects safety or habitability (burst pipe, broken heating in winter)

- Unexpected travel required for a family emergency

These do not qualify:

- Upgrading a device or appliance that still works

- A sale on something you have been wanting

- A vacation or leisure trip

- Holiday gifts or seasonal spending

- Planned or predictable expenses you forgot to budget for

💡The test is simple: is this expense unexpected, necessary, and genuinely urgent? If the answer to all three is yes, the fund is appropriate. If any one of those is no, it likely belongs in a different savings category or a future budget.

After You Reach Your Goal

When you reach your emergency fund goal, try to keep saving. You can add a little more or start saving for other goals like travel or investing. It’s also smart to grow your fund over time because of inflation — prices of goods and services keep going up, so the same amount might not be enough in the future.

Even after reaching my goal, I kept a small monthly addition running. Knowing that the fund’s value would hold up against rising costs over time gave me more confidence in it as a genuine safety net.

How long does it take to build an emergency fund?

It depends on your income, expenses, and monthly contribution amount. Saving $200 per month toward a $6,000 target takes 30 months. Saving $400 per month takes 15 months. Windfalls like tax refunds or bonuses can significantly shorten the timeline. Use the Emergency Fund Calculator to calculate your specific timeline.

Should I invest my emergency fund to grow it faster?

No. Emergency funds should stay in liquid, low-risk accounts. Investment accounts can lose value, and you may need the money during a market downturn. A high-yield savings account or money market account provides some growth while keeping the fund stable and immediately accessible.

What happens after I use my emergency fund?

Rebuild it as soon as financially possible. Treat it the same way you did when building it initially: set up automatic contributions and direct any available surplus toward restoring the balance. An emergency fund that gets used has served its purpose. The goal is to have it ready again before the next unexpected event.

Feel More Secure with Your Savings

Building an emergency fund brings real peace of mind and helps you feel more secure financially. The key is to start with what you can, keep at it regularly, and be patient. It’s also important to understand the difference between a rainy day fund and an emergency fund, as each serves a different purpose when managing unexpected expenses.

When I finally put mine together, I felt a lot more confident and less stressed about money. During tough times, I don’t freak out as much because I know there’s a safety net in place. You can get there too. Every little bit you save now can really pay off when life throws you a curveball.