Last updated on June 21st, 2026 at 11:05 am

Living on a fixed income means your money comes in the same amount, roughly the same time, every single month — and expenses don’t always return the favor. Whether you’re retired, on Social Security, receiving disability payments, or drawing from a pension, fixed-income budgeting isn’t about pinching every penny until it screams. It’s about building a system that fits your actual life, not one designed for someone still earning a growing salary.

This guide walks you through exactly how to do that — step by step, without the jargon, and without making you feel like you’re doing something wrong just by asking.

Step 1: Know Your Real Monthly Take-Home

Before anything else, you need a clear, honest number. Not an estimate — the actual amount deposited into your account each month.

For most people on a fixed income, that money comes from one or more of the following:

| Income Source | Notes |

|---|---|

| Social Security benefits | Check your SSA statement for the exact net amount |

| Pension payments | After any deductions for insurance or taxes |

| 401(k) or IRA withdrawals | If you take a regular monthly draw |

| Disability payments (SSDI/SSI) | Verified monthly net amount |

| Part-time or freelance income | Use a conservative, consistent average |

| Investment dividends or interest | Only count what’s predictable and recurring |

Write down the total net monthly income — that’s your ceiling. Everything else gets built around it.

Social Security payments do include a Cost-of-Living Adjustment (COLA) each year, but those increases rarely outpace what inflation does to groceries, utilities, and healthcare. That gap is real, and that’s exactly why having a retirement budget plan matters.

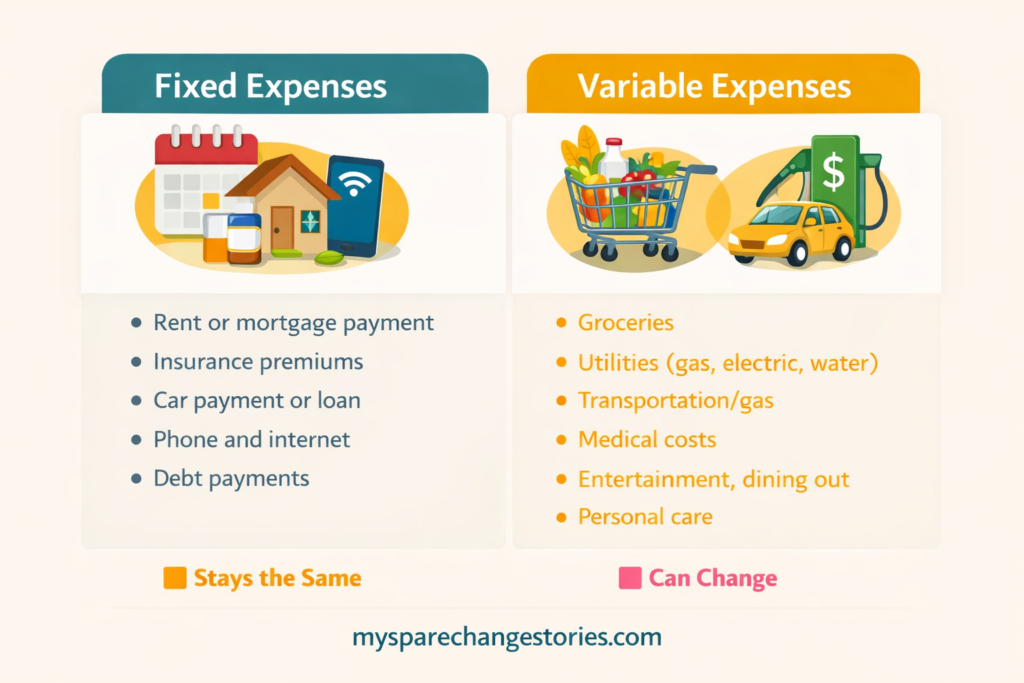

Once they’re sorted, you can see your guaranteed obligations clearly — and variable spending suddenly gets a lot easier to manage. If you want a deeper look at how to separate and handle these two categories, this guide on budgeting for fixed and variable expenses breaks it down even further.

Step 3: Apply a Budgeting Framework That Actually Works for Fixed Income

The classic 50/30/20 budget rule — 50% needs, 30% wants, 20% savings — was designed with a growing income in mind. On a fixed income, you’ll likely need to flip the script a bit:

A more realistic split might look like this:

| Category | % of Monthly Income | What Goes Here |

|---|---|---|

| Needs (Essentials) | 60–70% | Housing, food, utilities, Medicare costs, prescriptions |

| Wants (Quality of life) | 10–20% | Dining out, hobbies, subscriptions, entertainment |

| Savings / Buffer | 10% | Emergency fund, irregular expenses |

If 60% on needs sounds tight, it probably is — and that’s the point. When you can see that your essential vs. non-essential spending is out of proportion, you know where the problem is and you can actually do something about it. It’s not about judgment; it’s just math made visible.

Step 4: Build a Small Emergency Fund (Yes, Even Now)

The goal of three to six months of expenses in savings is a fine long-term target, but if you’re starting from zero, a more realistic first milestone is $500 to $1,000. Even that small cushion changes how it feels when the car needs a repair or a medical bill arrives unexpectedly. Without it, those costs go straight onto a credit card, which is one of the fastest ways to destabilize an otherwise manageable budget.

If you’re getting any kind of irregular income — a tax refund, a birthday check, a small freelance gig — the emergency fund is the best place for the first portion of it. That’s it. No formula required.

Managing debt alongside saving is also part of a stable fixed-income plan. The smartest move is to prioritize consistent, on-time payments over trying to eliminate debt fast, especially if cutting expenses on fixed income is already feeling tight. Avalanche or snowball methods both work; the best one is whichever you’ll actually stick with.

Step 5: Look for Assistance Programs You Might Be Missing

This is a step many people overlook — sometimes out of pride, and sometimes simply because they don’t realize these programs exist. But you deserve support, and there are legitimate federal and community programs created for exactly this stage of life. They’re not just for emergencies, and you don’t have to be in crisis to qualify. Think of them as resources meant to ease the load and give you a little more breathing room.

Food assistance:

- SNAP (Supplemental Nutrition Assistance Program) — Eligibility for seniors is often broader than people realize. In 2025, many recipients also saw a small increase in monthly benefits, and at participating farmers’ markets, SNAP benefits can go even further.

- National Council on Aging’s BenefitsCheckUp at benefitscheckup.org — This free tool shows you every benefit program you may qualify for, including food, housing, healthcare, and utilities.

Healthcare cost relief:

- Medicare Part D Extra Help — For those with limited income, this program through the Social Security Administration helps cover prescription drug costs.

- Many preventive services — flu shots, cancer screenings, diabetes tests — are covered at 100% under Medicare with no out-of-pocket cost when you stay in-network.

Utility bills:

- Many utility companies offer budget billing or levelized payment plans — meaning instead of a $180 gas bill in January and a $30 bill in June, you pay the same averaged amount every month. It won’t lower the total, but it makes budgeting utility bills on fixed income dramatically easier.

- Federal and state energy assistance programs (like LIHEAP) exist in most states for qualifying lower-income households.

Property tax relief:

- Homeowners 60 and older, or those retired due to disability, may qualify for property tax exemptions in their county. In many areas, only a small fraction of eligible seniors are enrolled — worth a quick call to your local assessor’s office to check.

Senior discounts:

- The National Parks Senior Pass ($20/year for those 62+) is one of the better deals almost nobody talks about.

- Many local transit authorities offer reduced or free fares for seniors and people with disabilities.

- Store loyalty programs, senior shopping hours, and prescription discount cards like GoodRx don’t require any application or income verification.

Step 6: Cut the Big Three — Housing, Healthcare, and Food

These three categories eat the largest share of most fixed-income budgets. Here’s where targeted attention pays off.

Housing

If you own your home, a good rule of thumb is budgeting about 1% of the home’s value annually for repairs and maintenance — so a $200,000 home means roughly $2,000 per year for the unexpected things that houses like to do.

If you’re a renter facing rising costs, a roommate arrangement, subsidized senior housing, or a move to a more affordable neighborhood might be worth exploring honestly.

Healthcare and Prescriptions

Preventive care is genuinely the most cost-effective thing here. A caught condition is far less expensive than a treated crisis. Beyond that, ask your doctor about generic alternatives whenever a new prescription comes up — the difference is sometimes dramatic.

And if you’re managing Medicare costs budgeting, supplemental (Medigap) coverage can help stabilize what’s otherwise a very unpredictable out-of-pocket picture.

Groceries

A grocery budget for seniors doesn’t have to mean eating worse — it usually just means shopping differently. Store brand items for pantry staples, loyalty apps with digital coupons, and buying proteins in bulk and freezing them cover a lot of ground. Curbside pickup also has an underrated benefit: you stick to your list. If you want practical strategies that go deeper, this piece on how to save money on groceries is worth a read.

Step 7: Track It Monthly and Adjust as You Go

A budget that isn’t reviewed is really just a list of good intentions. Once you’ve set yours up, check in at the end of each month and ask yourself: where did I overspend, and was it a one-time event or a recurring pattern? One costly month with a car repair is very different from consistently overspending on groceries — and each calls for a different response. You might even want to try the Kakeibo method — a Japanese approach to budgeting that blends numbers with reflection. It encourages you to ask not just what you spent but why, helping you spot patterns and make more mindful choices.

A monthly expense tracker doesn’t have to be complicated. A simple spreadsheet, a notebook, or free apps can all do the job. The best tool is the one you’ll actually use — not the fanciest one you’ll avoid. If staying consistent has been tough before, this guide on sticking to a budget offers practical tactics that make it easier to keep going month after month.

Budgeting Methods Worth Knowing

There’s no single right method for fixed-income budgeting. Here’s a quick look at the most practical options:

| Method | How It Works | Best For |

|---|---|---|

| Zero-based budgeting | Every dollar gets assigned a job until you reach $0 | People who want total visibility |

| Envelope budgeting method | Cash in physical envelopes per spending category | Those who overspend on variable categories |

| 50/30/20 | Percentage-based split, adjusted for your income | General structure for beginners |

| Pay-yourself-first | Savings comes out automatically before anything else | Building an emergency fund |