Last updated on June 22nd, 2026 at 01:06 pm

When I first started working, managing my paycheck felt confusing. I was excited to get my first salary but didn’t expect how fast it could disappear. It took time, trial and error, and a lot of honest reflection to build better habits. These 8 steps are what actually worked for me — and what I now do after every single paycheck.

1. Know Your Exact Take-Home Pay

The first step is knowing exactly how much money you actually have to work with — not what’s on your contract, but what lands in your account after every deduction.

Your gross pay is your total salary before deductions. Your net pay (take-home pay) is what’s left after taxes, social contributions, and any other withholdings your employer processes.

Depending on where you live and work, deductions might include income tax, health insurance, pension or retirement contributions, and social security. These can take a meaningful chunk out of your paycheck — sometimes 10–30% or more — so it’s important not to budget based on your gross salary.

For example, if you earn $3,000 per month before deductions, you might only take home $2,400–$2,600. That $400–$600 gap matters a lot when you’re planning down to the last dollar.

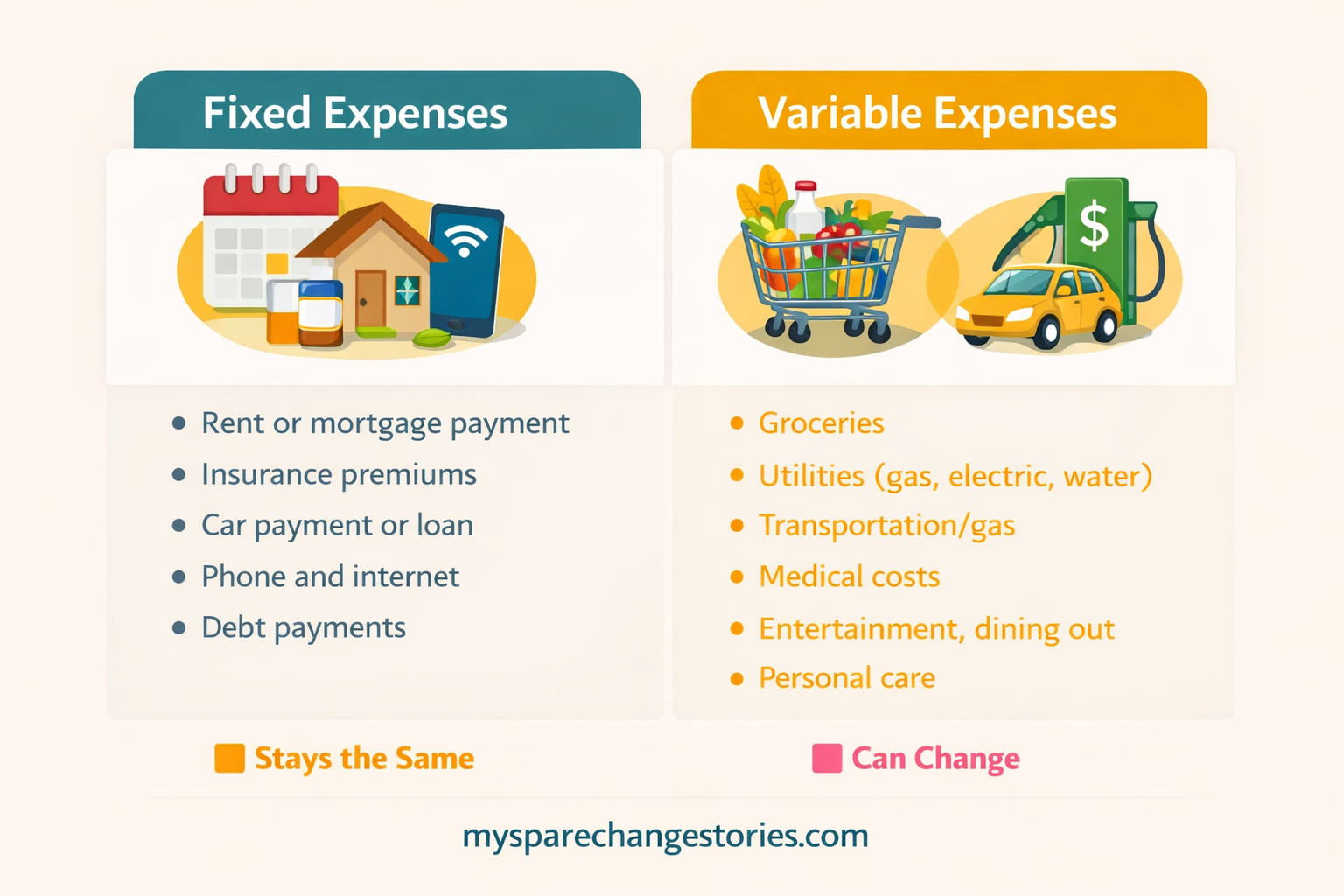

2. List and Categorize Your Expenses

Knowing where your money goes is super important. Split your expenses into two groups: fixed and variable. Fixed expenses are things like rent, utilities, and subscriptions that stay pretty much the same every month. Variable expenses are groceries, transport, and fun stuff that can change.

When I first did this exercise, I was shocked. I thought food was my biggest variable expense — but when I broke it down, it was food delivery specifically, not groceries. I was spending almost twice as much ordering in as I would have cooking at home. Seeing that on paper was the wake-up call I needed.

Whether it’s streaming subscriptions you forgot about, daily coffee runs, or impulse online shopping — the numbers don’t lie.

3. Set Short- and Long-Term Goals

Without clear goals, money tends to disappear into impulse purchases and vague “I’ll save next month” promises. Goals give your money a purpose.

Short-term goals (within 1–12 months):

- Covering all monthly bills on time

- Building a small starter emergency fund

- Paying off a specific debt

- Saving for a trip, gadget, or special purchase

Long-term goals (1 year and beyond):

- Building a full 3–6 month emergency fund

- Investing consistently

- Paying off all high-interest debt

- Saving for a major milestone — a home, a business, early retirement

Write your goals down. Assign a target amount and a deadline to each one. Vague goals stay wishes; specific ones become plans.

4. Choose a Budgeting Method That Fits You

Having a budgeting method helps structure spending and savings. Popular methods include:

| Method | How it works | Best for |

|---|---|---|

| 50/30/20 | Split your income into 50% for needs, 30% for wants, and 20% for savings or debt repayment. | Beginners who want a simple, no-fuss starting point Simple |

| Zero-Based | Every dollar gets assigned a purpose so that income − expenses = $0. Nothing goes unaccounted for. | Detail-oriented people who want full control over every dollar High control |

| Envelope System | Allocate fixed amounts into separate cash or digital envelopes per category. When an envelope is empty, spending stops. | Overspenders who need hard, visible limits on variable categories Spending limits |

| Pay-Yourself-First | Move money into savings immediately on payday — before spending anything. You live on whatever is left. | People who keep forgetting to save or always run out of money by month-end Savings-first |

I started with the 50/30/20 method — simple, clear, and easy to follow on a beginner’s salary. As my income grew and I kept my lifestyle relatively flat, I was eventually able to save up to 50% of my monthly income.

One tweak that worked for me: I set a fixed amount for “wants” each month. If I spent less than that, the leftover rolled over to the next month. It helped me save for bigger purchases without feeling deprived — a small habit that made a real difference.

💡 If you’re looking to understand budgeting better, take a look at our guides and tools for managing your money.

Explore Budgeting Calculators & Guides5. Pay Yourself First

This is probably the single most important habit on this list.

“Paying yourself first” means your savings are moved out before you spend on anything else — before shopping, dining out, or any non-essential expense. You treat savings like a non-negotiable bill that gets paid every payday.

Personally, I aim to save up to half my salary before I allocate anything for fun or extras. Not everyone can do that, and that’s perfectly okay. Even a small, consistent amount set aside every month is real, meaningful progress.

The psychology behind this matters: when you save first, the money is already “gone” from your spending mindset. You can’t accidentally spend what you’ve already moved to savings.

Practical ways to build this habit:

- Transfer to a separate savings account the day you get paid

- Set up an automatic transfer if your bank allows it

- Use a separate digital wallet or savings envelope so it doesn’t mix with your spending money

💡 Use our Savings Target Calculator to figure out how much to set aside each month to hit your goal.

Try Savings Target Calculator6. Pay Bills and Tackle Debt Strategically

Once savings are set, address your bills and debts — before anything optional gets a single cent.

For bills: Pay fixed obligations first — rent, utilities, insurance, loan payments. Set reminders or auto-pay where possible to avoid late fees and protect your credit.

For debts: If you have multiple debts, choose a strategy and stay consistent:

- Debt Avalanche: Pay minimums on everything, then direct extra money toward the debt with the highest interest rate. This saves the most money over time.

- Debt Snowball: Pay minimums on everything, then attack the smallest balance first. You get faster early wins, which helps keep you motivated.

Neither is wrong — the best strategy is the one you’ll follow through on. Keep a simple list of your debts: who you owe, how much, the interest rate, and the minimum payment. Update it monthly. Watching those numbers shrink is one of the most motivating feelings in personal finance.

7. Track Spending

Tracking spending helps stop overspending and makes you aware of your money habits.

Checking your expenses often keeps you on budget and focused on what matters. Since I love tracking my spending, I found out most of my money went to food, which helped me change my habits.

8. Reflect and Adjust Every Month

This final step is what separates people who budget once from people who actually build lasting financial habits: reflection.

At the end of each month, ask yourself:

- Did I stick to my budget? Where did I overspend?

- Did I hit my savings goal?

- What worked well? What felt too restrictive?

- Is there a spending pattern I keep repeating?

This is the core idea behind the Kakeibo method — the Japanese budgeting philosophy that emphasizes mindfulness and self-reflection, not just number tracking. Instead of simply logging transactions, Kakeibo encourages you to pause and honestly evaluate your financial decisions and what drives them.

Monthly reflection turns your budget from a static document into a living system that improves over time. It also keeps you focused on your progress — not what people around you seem to be spending.

Final Thoughts

Here’s the truth: managing your paycheck will never be perfect, especially at the start. You’ll overspend some months. You’ll forget to track. You’ll make purchases you later regret.

That’s okay. The goal isn’t a flawless budget — it’s building habits that move you in the right direction over time.

Start with just one or two steps from this list. Know your take-home pay. Set aside even a small amount in savings. Track your spending for 30 days. Small, consistent actions compound into real financial stability.

Your financial journey is your own. Your income, your goals, your pace. Take it one paycheck at a time.