Last updated on June 26th, 2026 at 01:26 am

January shows up every year with big “new era” energy, usually right after December has emptied both your wallet and your willpower. You open banking apps you avoided all holiday season, mentally subtracting food deliveries, forgotten subscriptions, and that one purchase no one can quite explain.

Saving money does not mean becoming a completely different person with color-coded spreadsheets and monk-level discipline. It means finding one small rule, one simple experiment — a challenge that fits into your real life, the kind you can follow even when motivation fades somewhere between your third coffee and your first forgotten resolution.

This list has 22 money-saving challenges, organized by type, each with an honest look at how it works, how much you could realistically save, and what kind of person it suits best. You do not need to do all of them. Pick one. Start this week.

Time-Based Saving Challenges

These challenges use the calendar as your structure. No complicated budgets, just a rule tied to time.

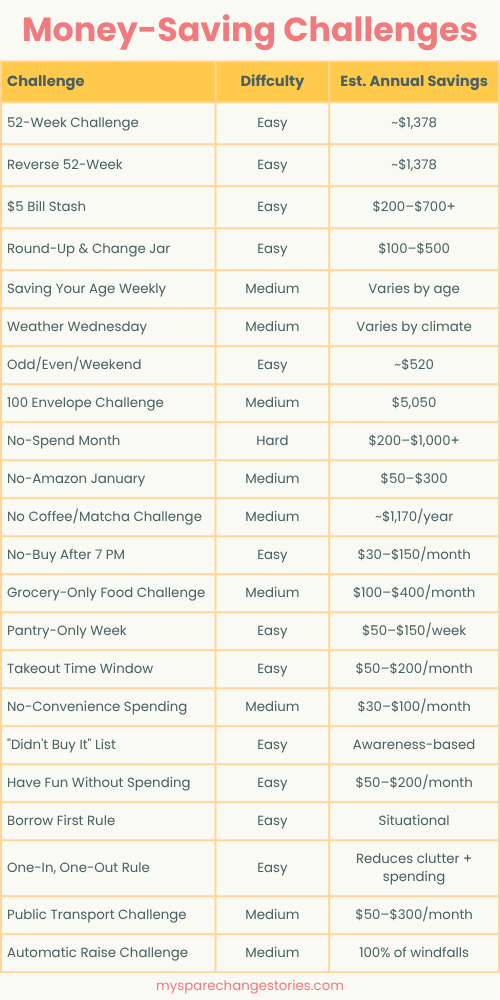

The 52-Week Saving Challenge (and the Reverse Version)

This is the classic. It starts modestly and builds each week until the end of the year, feeling manageable in January and more demanding as the months go on.

How it works: Save $1 in week one, $2 in week two, $3 in week three, increasing by a dollar each week until week 52.

The reverse version starts with $52 in week one and decreases by $1 each week. This front-loads savings when your motivation is highest and eases off as life gets busier. It works particularly well for people with irregular income or those who tend to lose steam mid-year.

How much you’ll save: $1,378 either way, by the end of the year.

Best for: Beginners who want a clear, pre-set structure with no guesswork.

💡 Use our Savings Target Calculator to see how these weekly deposits build toward a bigger goal.

Try the Savings Target CalculatorSaving Your Age Each Week

A subtle, slightly playful way to tie savings to where you are in life.

How it works: Each week, save an amount equal to your age. If you are 28, set aside $28 per week. If you turn a year older mid-challenge, adjust the amount to match.

How much you’ll save: At age 28, that is $1,456 a year. At 35, it is $1,820. The amount scales naturally as you get older, which gives this challenge a longer lifespan than most.

Best for: People who want a personalized weekly amount without doing fresh calculations each month.

The Weather Wednesday Challenge

Specific, unpredictable, and interesting enough to hold attention across different seasons.

How it works: Every Wednesday, save an amount that matches the temperature forecast for the day. If it is 68°F, save $68. If you prefer Celsius, save $20 on a 20°C day. Pick a unit and stick to it.

How much you’ll save: Anywhere from $500 to $2,000+ over a year depending on your climate and which unit you use.

Best for: People who get bored with rigid saving schedules and want something with variability built in.

The Odd/Even/Weekend Challenge

Savings follow the calendar instead of a schedule you have to actively manage.

How it works: Save $1 on odd-numbered days, $2 on even-numbered days, and $5 on weekends. Check the date, transfer the amount, move on.

How much you’ll save: Approximately $520 over a full year, in small increments that rarely feel like much on any given day.

Best for: Anyone who wants a low-effort daily habit that runs on autopilot.

Spending Restriction Challenges

These challenges do not set a savings target directly. They restrict a specific type of spending, and savings happen as a natural result.

The No-Spend Month

One of the most searched saving challenges for a reason. Done well, it is less about deprivation and more about awareness.

How it works: For one full month, spend only on true necessities: rent, utilities, groceries, transport, and essential bills. Dining out, online shopping, entertainment subscriptions, and impulse buys are off the table for the duration.

Tips to actually finish it:

- Choose a slower month like January or February when there are fewer social commitments

- Write out your “allowed” and “off-limits” categories before you start, so there is no grey area mid-month

- When the urge to spend hits, write the item down on your “Didn’t Buy It” list instead (more on that below)

- One slip-up does not end the challenge. Keep going.

How much you’ll save: $200–$1,000+ depending on your usual spending habits.

Best for: People who want a hard reset after a high-spend season, or anyone who cannot figure out where their money goes each month.

If you want to take it further, pairing a savings challenge with a no-buy list makes the whole thing easier. Here are 27 things I’m not buying in 2026 if you need a starting point.

The No-Amazon January Challenge

January is a natural low-energy month, which makes it a good window to cut off impulse delivery entirely.

How it works: No online shopping from Amazon (or whichever platform you default to) for the entire month. No scrolling, no adding to cart to “compare later,” no ordering.

What the challenge tends to reveal is how often online shopping fills boredom rather than genuine need. Most items that feel urgent at 10 PM lose their appeal a few days later.

How much you’ll save: $50–$300 depending on your current ordering frequency.

Best for: Online shoppers who notice their packages arriving more often than they remember ordering.

The No-Buy After 7 PM Challenge

Late-night scrolling and tired decision-making are a poor combination. This challenge draws a firm line.

How it works: No purchases of any kind after 7 PM. Groceries, snacks, apps, online orders — all of it waits until the next day.

Decision fatigue is well-documented. Your ability to evaluate whether you genuinely need something is worse at 10 PM than it is at 10 AM. The 7 PM cutoff protects you from decisions made when your judgment is most depleted.

How much you’ll save: $30–$150 per month depending on how often you shop or order in the evenings.

Best for: People who order food or shop online late at night, or who wake up to purchases they do not fully remember making.

The No-Convenience Spending Challenge

This challenge targets the smallest, most invisible spending: purchases that exist purely to make life a few seconds faster.

How it works: For a set period, cut convenience spending. No bottled water when you have a reusable bottle, no snacks grabbed near the register, no fees paid to skip a queue or speed up shipping.

For example, if you spend $2 on a bottled drink three times a week, removing that one habit saves $312 over a year.

How much you’ll save: $30–$100 per month once you start recognizing these micro-purchases.

Best for: People who feel like their major spending is under control but still cannot account for where money goes.

Food and Lifestyle Challenges

Food is the category where most people have the widest gap between what they spend and what they think they spend. These challenges close that gap.

The No Coffee or Matcha Challenge

Not forever. Just long enough to see how much of a daily routine runs without conscious thought.

How it works: Skip café-bought coffee, matcha, or your usual drink for a set period. One month is a solid starting point. Make it at home or skip it for the duration.

How much you’ll save: If a drink costs $4.50 and you buy one five days a week, that is $22.50 per week, or roughly $1,170 per year. Cutting back to twice a week still saves over $700 annually.

Beyond the money, the challenge creates a moment of awareness each time you almost place a familiar order. That pause tends to make the habit feel less automatic even after the challenge ends.

Best for: Daily café regulars who have never calculated what their habit costs across a full year.

The Grocery-Only Food Challenge

All food comes from a grocery store. No exceptions, no grey areas, no delivery apps.

How it works: For one month, if it is not available at a grocery store, it does not get bought. This includes deli counters, frozen meals, and prepared grab-and-go items — convenience is still available, just through a different channel.

How much you’ll save: $100–$400 per month depending on how often you currently eat out or order delivery.

Best for: People who know they overspend on food but have not pinpointed exactly where.

The Takeout Time Window Rule

Takeout is not banned. It just gets a schedule.

How it works: Choose a specific window when ordering food is allowed, for example 11 AM to 2 PM only. Outside that window, you cook or eat what is already available.

Most impulse food orders happen in the evening. Limiting orders to a daytime window turns them into deliberate choices rather than tired reflexes. You may find you order less often, not because of restriction, but because planning ahead removes a lot of the appeal.

How much you’ll save: $50–$200 per month depending on your current ordering habits.

Best for: People who order takeout more out of habit or exhaustion than genuine preference.

The Pantry-Only Week

A week built entirely around what is already in your kitchen.

How it works: Before your next grocery run, spend one full week eating only what you already have, including items pushed to the back of the pantry, the freezer, and the fridge. No store trips, no backups, no “I just need one thing.”

Most households have considerably more food than they realize. The pantry-only week turns forgotten ingredients into usable meals and reframes food spending as something already done rather than a constant, ongoing task.

How much you’ll save: $50–$150 for that single week, plus whatever would have expired unused.

Best for: Anyone who regularly throws away food or shops more frequently than they probably need to.

Mindset and Habit Challenges

These challenges ask you to change how you think about spending. The savings follow from that shift.

The “Didn’t Buy It” List Challenge

Instead of tracking what you spend, this challenge tracks what you chose not to spend.

How it works: Every time you resist buying something non-essential, write it down with the price. That is the entire system. No apps, no budgets, no complicated tracking.

After a few weeks, the list becomes more interesting than any receipt. You start to see patterns in what you almost bought and did not. The pause before a purchase becomes a habit in itself, and habits outlast willpower.

How much you’ll save: Awareness-based, but many people find this challenge reveals $100–$300+ in near-misses per month once they start paying attention.

Best for: Anyone who struggles with impulse purchases, or who has tried budgeting apps and found them more stressful than helpful.

The Have-Fun-Without-Spending Challenge

This one tends to surface organically after noticing how many social plans involve spending by default.

How it works: For a set period, find ways to enjoy yourself that cost nothing — free walks, movie nights at home, borrowed books, shared playlists, park visits, long conversations that do not require a reservation.

The goal is to discover how much enjoyment is already available without a purchase attached to it. Most people find more than they expected.

How much you’ll save: $50–$200 per month depending on your usual social spending.

Best for: People who feel like they need to “go somewhere” or “do something” to enjoy free time, or anyone whose social life costs more than they are comfortable with.

The Borrow First Rule

Ownership stops being the automatic answer.

How it works: Before buying any item, especially one you will use rarely, ask if you can borrow it. Borrow a drill from a neighbor, check a book out from the library, use a friend’s kitchen gadget instead of buying your own.

Most things people buy get used a handful of times and then sit unused. The Borrow First rule surfaces a genuine question before each purchase: do you need to own this, or do you just need access to it?

How much you’ll save: Situational, but particularly effective for tools, equipment, specialty kitchen items, and books.

Best for: People who tend to buy items for one-time projects or occasional use.

The One-In, One-Out Rule

Every new item replaces something that already exists.

How it works: When you buy something new, one existing item of the same type leaves. Donate it, sell it, or give it away. New jacket in, old jacket out. New skincare product in, old one out.

The friction of identifying what you would replace is often enough to reveal whether you actually need the new item. Buying slows down without requiring a hard ban on anything.

Best for: People who feel like they have too much already but keep adding more, or anyone trying to shift toward more intentional spending.

Physical and Passive Saving Challenges

These challenges work in the background. Once the habit is set, they require very little active decision-making.

The $5 or $10 Bill Stash Challenge

There is something satisfying about treating physical cash as though it does not exist the moment it arrives.

How it works: Every time you receive a $5 or $10 bill (or whichever denomination you choose), it goes straight into a dedicated drawer, envelope, or pouch — untouched and uncounted until you decide the challenge is over.

How much you’ll save: $200–$700+ over a year depending on how often you use cash. It tends to surprise people when they finally count it.

Best for: Cash users who want a completely passive saving habit with no tracking required.

The Round-Up and Change Jar Challenge

Small leftover amounts from daily purchases rarely register in the moment, but they add up over months.

How it works: Each time you make a purchase, round up to the nearest dollar and set aside the difference. If your coffee costs $3.47, that $0.53 goes into a jar or a savings app. Physical loose change from cash purchases goes in too.

How much you’ll save: $100–$500 over a year, depending on how often you spend and whether you use a round-up app.

Best for: People who want a saving habit that runs without conscious effort.

When I was a student, I bought a coin bank I loved so much I refused to open it until it was completely full. That one rule — wait until it is full — was enough to keep me from raiding it for months at a time.

It looked exactly like this!

The 100 Envelope Challenge

A mix of randomness and structure that many people find more engaging than fixed schedules.

How it works: Label 100 envelopes with amounts from $1 to $100. Each day or week, pick one at random and deposit exactly that amount. Over time, every envelope gets filled.

How much you’ll save: $5,050 total, which is the sum of every number from 1 to 100, by the time all envelopes are complete.

Best for: People who enjoy a tangible, visual saving system and find randomness more motivating than a fixed plan.

You might also like: How Does Envelope Budgeting Work?

The Automatic Raise Challenge

Any unexpected money — bonuses, tax refunds, freelance payments, cash gifts — goes to savings before it touches your spending account.

How it works: The moment any extra money arrives, transfer it to savings immediately. It moves before habits have time to adjust and before it starts to feel like available spending money.

Over a full year, these windfalls often add up to more than people realize, partly because they tend to disappear into regular spending without leaving much trace.

Best for: Anyone whose income occasionally spikes but who cannot figure out where the extra amounts went afterward.

The 48-Hour Holding Period Rule

This one barely registers as a challenge until you notice how rarely you complete purchases after waiting.

How it works: Anything non-essential waits 48 hours before checkout. Add it to your cart, screenshot it, save it for later — just do not buy it for two full days.

In most cases, the urge passes on its own. The item moves from “want” to “do not actually care about” without any active effort. The rule works by outlasting the impulse rather than fighting it.

How much you’ll save: Highly variable, but research on impulse buying consistently shows that waiting periods eliminate a significant share of unplanned purchases.

Best for: Online shoppers or people who add to cart as a form of stress relief.

The Public Transport and Walking Challenge

For a set period, transport sticks to public options or walking. Ride-hailing apps stay closed unless the situation genuinely requires it.

How it works: Decide on a timeframe — one week or one month — and commit to buses, trains, cycling, or walking as your default. Ride-sharing becomes a last resort rather than a first instinct.

Beyond the savings, the challenge tends to change how days get planned and how often convenience gets chosen without thinking.

How much you’ll save: $50–$300 per month depending on your city, commute, and current transport habits.

Best for: People in cities with reliable public transport, or anyone who uses ride-hailing apps more out of habit than necessity.

How to Choose Your Challenge

If you are staring at this list feeling uncertain about where to start, here is a simple way to narrow it down:

If you want to save a specific, predictable amount — try the 52-Week Challenge or 100 Envelope Challenge.

If you tend to lose motivation partway through the year — try the Reverse 52-Week or Odd/Even/Weekend Challenge.

If you overspend on food — try the Grocery-Only Challenge or Takeout Time Window.

If impulse buying is the main problem — try the 48-Hour Rule or the “Didn’t Buy It” List.

If you want savings to happen with minimal thinking — try the Automatic Raise Challenge or the Round-Up Jar.

If you are not sure where your money actually goes — try the No-Spend Month. Few things reveal spending patterns faster.

Turn 2026 into a Year of Smart Savings

By the end of a year of small experiments, the results tend to show up in places you did not expect: coins in jars, old habits shifted, savings in accounts you almost forgot about.

None of these challenges ask for perfection. They ask for a willingness to notice patterns that have been running on autopilot and to make slightly different choices, one week or one payday at a time.

Pick one. Start this week.

If you are building savings momentum, these simple financial resolutions for better money habits are a natural next step.